Background

Power procurement accounts for nearly 70% of the total expenditure of distribution companies (Discoms). Given this high share, any fluctuation in procurement costs arising from variations in fuel prices, generation mix, transmission charges, or market dynamics has substantial downstream implications. Even a marginal increase can significantly affect the average cost of supply (ACOS) and, consequently, the retail tariffs. When these cost variations are not fully passed through to consumers, the resulting mismatch contributes to revenue gaps and adds to the financial stress and accumulated losses of the Discoms.

GST Reforms and their Impact on the Power Sector

In this context, the decision taken at the 56th meeting of the GST Council in September 2025 to implement next-generation reforms to the eight-year-old GST regime has significant implications for state Discoms. These reforms revise the tax and cess structure for both interstate and intrastate coal supplies. Since coal remains the dominant fuel in India’s energy mix, this measure could lower production costs for thermal generators and, in turn, ease the cost burden on Discoms, marking a rare instance where policy intervention has led to a reduction in coal procurement prices.

In 2017, the Parliament enacted four laws, namely the Central Goods and Services Tax (GST) Act, 2017, the Integrated Goods and Services Tax (GST) Act, 2017, the Union Territories Goods and Services Act, 2017, and the Goods and Services Tax (Compensation to States) Act, 2017, to replace the previous indirect tax regime. Before the introduction of the GST, states collected various indirect taxes, such as VAT, CST, and entry tax. With the rollout of GST, these sources were subsumed under a unified regime, reducing states’ independent revenues. The Goods and Services (Compensation to States) Act, 2017, provided for a mechanism for compensation to the states for loss of their revenues by imposing a GST Compensation Cess of ₹400 per tonne of coal supplied. Now, as part of the rationalisation process in the 56th meeting, the Council has now withdrawn this cess and has merged its burden into GST, thereby raising the GST rate on coal from 5% to 18%. The removal of the compensation cess offsets the increased tax burden for all coal priced at ₹3,076 per tonne or less. According to current notifications, Grade G-11 coal (the most common grade of used coal in India) is priced at approximately ₹1,815 per tonne under Fuel Supply Agreements (FSA) and around ₹2,533-2,671 per tonne through e-auctions. Therefore, the net impact of the cess removal remains beneficial for many power plants using this grade or lower.

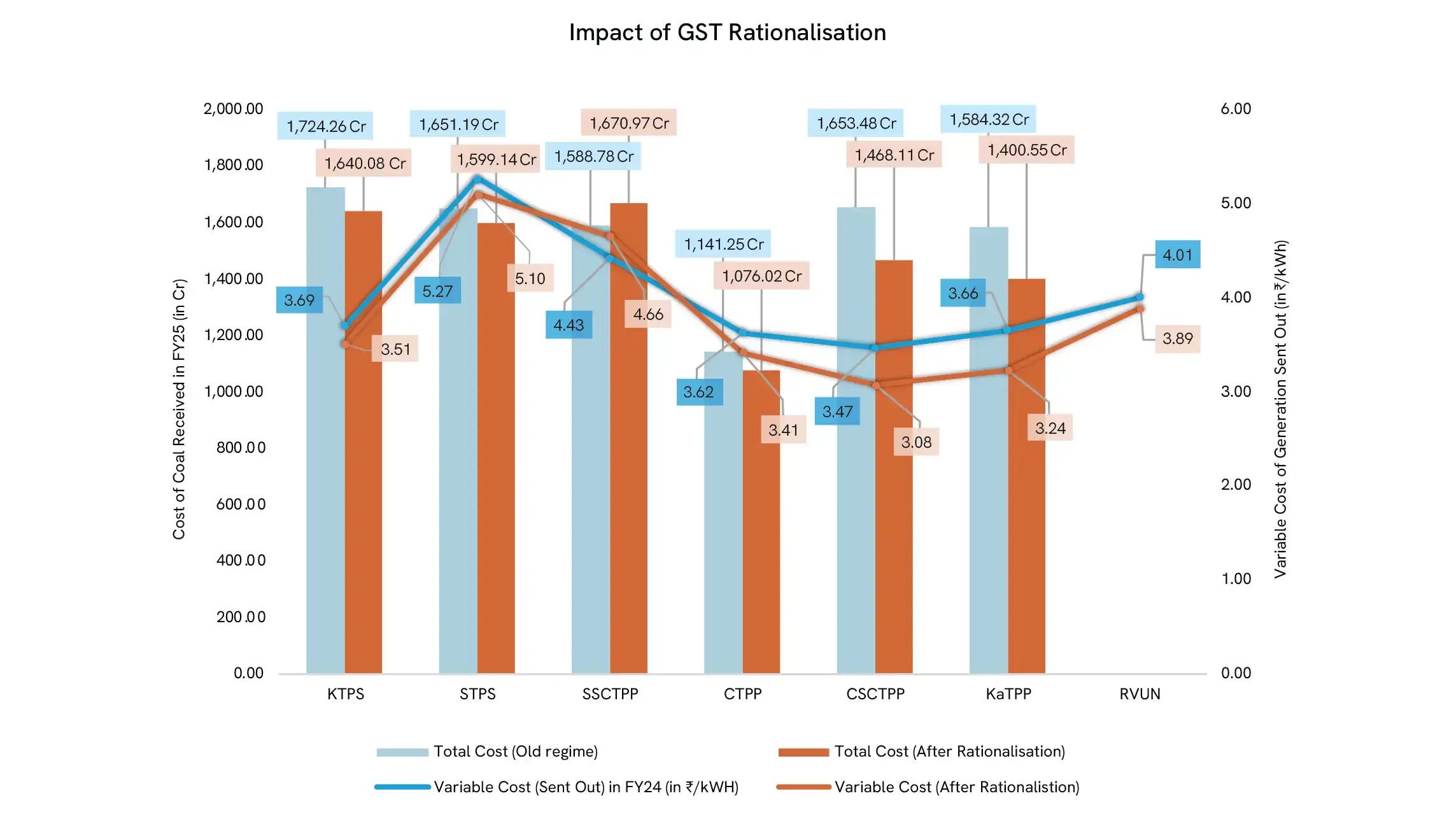

Case: Rajasthan

In Rajasthan, taking the case of the state electricity generation company, Rajasthan Vidyut Utpadan Nigam Ltd. (RVUNL), sourced nearly 30% of its fuel from captive mines in Chhattisgarh, while the remaining was purchased from Coal India Limited (CIL) during the financial year 2024–25. Until now, RVUNL has been paying 5% GST and a compensation cess on coal purchased from CIL, and 18% GST along with the compensation cess on coal sourced from its captive mines. The new regime results in a direct cost reduction of ₹400 per tonne for coal sourced from captive mines, resulting in an overall saving of about 12.67% on such coal. For coal procured from CIL, which constitutes nearly 70% of total purchases, the cost saving is around 4.55%. The utility achieves an overall cost saving of approximately 5.23% from both captive mines and CIL, reflecting the combined impact of the reduced cess across its total fuel mix.

It is important to note that the change in the tax regime will affect each RVUNL plant differently, as the source of coal and coal types vary across its six coal-based power plants (with subcritical and supercritical units considered separately) (Figure 1). With each plant having different operational parameters (such as station heat rate, specific consumption, availability, load factor and units sent out), the variable cost of electricity sent out from the plants may vary significantly. The costs may vary anywhere from an increase by nearly 20 paise per unit (as seen in the case of Suratgarh Supercritical Thermal Power Plant) to a reduction of approximately 30-40 paise per unit (as noted in case of Kalisindh Thermal Power Plant and Chhabra Supercritical Thermal Power Plant, which have a better savings due to a higher share of fuel from captive mines). At the RVUNL level, considering the weighted average of electricity supplied by each plant, the overall savings amount to roughly 12 paise per unit.

Regulatory Implications

Rajasthan’s Discoms should promptly notify these changes to relevant parties, including generators and coal suppliers, and direct them to pass on the benefit under the change-in-law provision. In the absence of suo motu action by the regulator, they should also file petitions before the appropriate commission to mandate the pass-through of these benefits. The Central Electricity Regulatory Commission (CERC) has already initiated a suo motu petition inviting comments on the abolition of the GST Compensation Cess and the increase in the GST rate on coal procurement, aiming to establish a uniform regulatory approach for addressing these change-in-law events and to facilitate the settlement of related dues across PPAs under its jurisdiction.

Policy Recommendations

Passing on these benefits to Discoms would help lower retail tariffs, strengthen their financial health, and create greater fiscal space for investments in grid modernisation and renewable energy integration. As an alternative, the savings can be used to reduce the state’s regulatory assets, further strengthening the financial stability and operational efficiency of the distribution sector. The three Discoms of Rajasthan have accumulated regulatory assets of nearly ₹44,257 crore, as noted in the RERC tariff order for FY 2025–26, which are to be recovered over the next two financial years in accordance with the recent Supreme Court directive. This translates to an additional burden of approximately ₹2-2.30 per unit for consumers. Given this situation, the Discom may request the Rajasthan Electricity Regulatory Commission not to pass the savings of roughly 12 paise per unit directly to consumers, but instead use them to offset the projected increase in tariffs needed to liquidate regulatory assets.

Overall, the GST Council’s coal tax reforms offer a rare opportunity to ease Discoms’ cost pressures and strengthen their financial position. Though immediate gains for consumers may be tempered by regulatory imperatives, the long-term impact could help stabilise tariffs, reduce liabilities, and create fiscal space for investments in reliability and clean energy integration.

The article is authored by Anshuman Gothwal, Co-founder and Director-Programs at CEEP, and Manish Kumar Mahto, Senior Research Associate at CEEP.

Please ensure all required fields (*) are filled out accurately.